DEAL IN FOCUS: NOVENTIQ – CORNER GROWTH ACQUISITION CORP. (COOL)

|

Chart 1: Noventiq at a Glance |

|

|

Source: Intro-act, COOL/Company Investor Presentation. FY22 ended 3/31/22, FY23 year ended 3/31/23, FY24 year ending 3/31/24: $ in USD

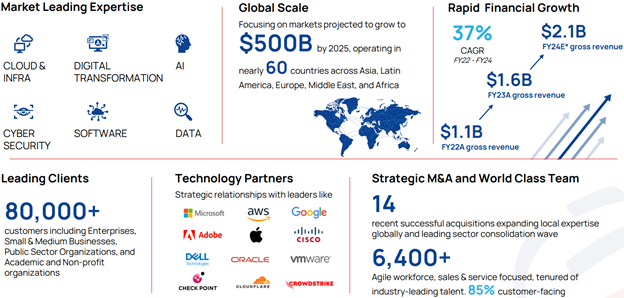

Noventiq’s strategic partnerships strengthen its growth strategy and extend its competitive reach. As a top partner for global public cloud companies, including Microsoft, AWS, and Google, Noventiq has built strong relationships over the last 25 years, establishing itself as a leading strategic partner in various growing markets. The company aims to expand its services and deliver partner technologies as part of its customer-focused solutions portfolio. The company accelerates its value creation as a consolidator with a successful merger and acquisition track record. Since 2020, it has acquired 14 companies. Its approach focuses on strategic expansion in terms of market, capabilities, portfolio, and sales channels. Looking ahead, Noventiq anticipates continued topline and margin growth through expanding its services business and introducing new product lines and categories, including enterprise-grade smart assistants powered by generative AI and other next-gen products from their partners (e.g., Microsoft). These initiatives serve as key drivers for expanding high-margin solutions via its land and expand model.

|

Chart 2: Noventiq Is a Leader in The Digital Transformation |

|

|

Source: Intro-act, COOL/Company Investor Presentation

Noventiq has displayed a proven ability to grow rapidly in emerging markets. The company recorded gross revenue of $1.6 billion in FY23 (fiscal year ended 3/31/23), up by 40% in US Dollar terms, and 52% in constant currency. This was driven by gross revenue growth across geographies, with double-digit increases across all four regions in FY23, including strength in India. For FY24, the company is targeting gross revenue of at least $2.1 billion, representing at least 34% growth in reported currency. This level of gross revenue growth would represent almost doubling the size of the business over two years. In FY24, the company is targeting gross profit of $240 million, which would represent 36% growth, and adjusted EBITDA of $65 million, which is a 27% margin on gross profit. Based on the timing impact of investments, and the seasonality of its business, Noventiq expects adjusted EBITDA margin to be lower than the full year range in the first half of the year and higher in the second half.

Chart 3: Demonstrating Fast Growth and Profitability at Scale |

|

|

Source: Intro-act, COOL/Company Investor Presentation. 1. Pro-forma adjustments for standalone costs originally allocated to the divested business and full year impact of closed acquisitions, 2. Pro-forma adjustments for full year impact of closed acquisitions, 3. Includes application of IAS 8 to restate Services costs into COGS, 4. Excludes Depreciation, Amortization and One-time expenses. Fiscal Year End = 3/31.

In May 2023, Noventiq and Corner Growth Acquisition Corp. (Nasdaq: COOL) announced their business combination and in June published their investor presentation; the transaction values the company at $650 million (enterprise value). Upon closing of the transaction, and assuming no stockholders of Corner Growth redeem their shares, Noventiq will have $210 million pro forma cash on its balance sheet, consisting of $100 million in anticipated new financing proceeds and $135 million in existing cash (as of 3/31/2023), less $25 million in transaction fees. Following completion of the business combination, existing Noventiq shareholders are expected to own 82.2% of the fully diluted shares of the combined company, with public stockholders of Corner Growth expected to own 11.9%, and the Sponsors expected to own 5.9%.

§ Upon the closing of the transaction, the combined company will be named Noventiq. It is expected to be listed on Nasdaq under the ticker symbol NVIQ and close in 2H23.

|

Chart 4: Transaction Summary |

|

|

Source: Intro-act, COOL/Company Investor Presentation

Q&A OF THE MONTH – JAY JACKSON, CEO OF ABACUS SETTLEMENTS

The Ambitious Plans of a Life Settlement Company Going Public

The CEO of Abacus Settlements expects that becoming publicly traded will expand the secondary market for life insurance. And that could mean stiff competition for insurers that buy back policies via surrenders.

Abacus Settlements CEO Jay Jackson says the company is on track to become the first publicly traded life settlement company this year. He expects that would give it a platform to bolster purchases of life insurance policies on the secondary market. That could intensify competition between life settlement companies and life insurers that collect billions of dollars yearly off contracts that are surrendered.

The company, which does business as Abacus Life, would become public by merging with Longevity Market Assets, a buyer of life insurance policies, and East Resources Acquisition, a “blank check” company established to merge with or buy other companies. The deal is expected to close on 6/30 with a 7/3 first trading date.

Jackson shared his perspective on the market and the company’s campaign to entice more advisors and agents to sell their clients’ policies to Abacus in a Q&A with Life Annuity Specialist.

The following was edited for length and clarity.

Q: What’s the status of Abacus’s merger agreement, which will enable you to become a public company?

A: We have until July 27, per our last extension in January. So, we’re very optimistic that it will be closed before that extension expires.

Q: What will you be able to achieve as a publicly held business that you couldn’t as a private company?

A: The biggest thing we’re trying to accomplish is to raise awareness for our industry and our asset class. As a public company, because we will now be totally transparent in every transaction that we do, that builds a higher level of trust with people who are considering selling their policy or investors who might want to invest in this asset.

We estimate that, in 2023, $250 billion in policies will lapse without insureds and policyholders knowing that this financial option exists for them.

Q: And you’ll have more capital with which to buy policies?

A: That’s right. It gives us access to more capital at a lower cost.

Q: Will the institutional investors that are behind you — hedge funds, private equity firms, banks — continue to play a role, supplementing the capital being raised on the public markets?

A: Yes. We will still work with all our institutional partners and consistently make sure that they have the investment opportunity. In fact, what this does — by being a public company — it opens up origination. If we increase origination [of life settlements], we can provide more policies for those investors to purchase. A major complaint of institutions is that they go out and raise $1 billion to place in the asset, and they can’t find any policies to buy.

Q: How would you differentiate Abacus from competitors? Will you be one of the few life settlement companies that’s gone public?

A: When we go public, we will be I think the only life settlement provider — the only origination company — that’s public. And that places us under a much higher level of scrutiny than other companies that are not public.

Q: Can we expect other initiatives once you are a public company?

A: We launched our television campaign in January, which is focused specifically on using our life settlement calculator. All that users have to do is put in their gender, age, value of their policy and policy type. And, instantly, they receive a potential valuation based upon what they deem their health to be.

Secondly, we are running that commercial in the morning on CNBC, Bloomberg, and Fox Business to educate and advise financial professionals that this opportunity also exists, not just for their clients. We’re asked frequently, “Why don’t you just advertise to seniors on the Golf Channel or the Weather Channel?” We know that almost every life insurance policy is sold through an insurance agent or advisor. We need to educate them as well.

Q: Will these agents and advisors partner with life settlement brokers affiliated with Abacus?

A: An insurance agent or advisor can come to us directly.

Q: How many agents and advisors are now affiliated with Abacus? And how many more do you hope to recruit?

A: We’re don’t require an affiliation. Agents and advisors are free, once they’re licensed, to send that policy to whomever they choose.

We work with tens of thousands of insurance agents and financial advisers across the country. We are licensed in nearly every state that requires it.

Q: Coming back to the calculator, how much more on average might a customer receive for a life settlement from Abacus than by surrendering their policy to the issuing insurer for the cash value?

A: In 2022, our calculated payout was eight times higher than the client’s cash surrender value on average. That’s consistent with prior years, and the differential has been driven by a couple of things. Carriers have been faced with a low interest rate environment, so cash values have been depressed. On a go-forward basis, we will probably see that gap shrink a bit as interest rates go higher. The multiple may come down to six times the cash value, but it’s still significant.

Q: Are you seeing a shift in the reasons why a senior might want to sell a policy?

A: What we see today is different than what we saw 10 years ago. The life settlement is truly an estate planning tool today. The financial need could be a factor. But we think a much larger factor is people who are doing estate planning. They’re thinking about how they can utilize that liquidity today for their estate.

So, a higher proportion of life settlements are tied to estate planning. We’re also seeing an increase in the size of the policies people are selling. Traditionally, the average face amount was less than $1,000,000. Now we regularly see from $2 million to $20 million.

Q: Does that in part reflect your distribution strategy — working more with agents and advisors who are catering to wealthier folks?

A: That’s exactly right.

Q: What are the implications for the life settlement industry of current economic and business conditions, including financial strains in the banking sector?

A: We have seen a continuous, steady increase in inquiries from people. And I think that’s a natural effect of any fear in the market among people looking for liquidity.

Q: Has the transition to going public entailed adding staff?

A: We’ve increased our staff by about 20% in the trailing 12 months. We’ve seen an increase in the number of policies that we’ve purchased over the same period, so we’ve matched staff to accommodate that. But in addition, we’ve added staff to help manage the public company process.

Link to original interview: https://abacuslifesettlements.com/qa-the-ambitious-plans-of-a-life-settlement-company-going-public/

U.S. de-SPAC & SPAC data & statistics roundup. U.S. de-SPAC M&A value made steady year-on-year gains in Q1 2023, with deal value of $9.94 billion coming in 37% higher than Q1 2022 figures. The year-on-year rally in de-SPAC deal value in Q1 2023 stood in contrast to overall global M&A, which recorded the third lowest quarterly M&A value for 10 years, with only $559 billion worth of transactions posted during the first three months of 2023, according to Bloomberg. One of the reasons why de-SPAC M&A activity has bucked broader M&A trends has been the race by SPAC sponsors to close deals before investment periods expire. Read More (JD Supra)

|

Chart 5: Annual Summary of de-SPAC Transactions in the U.S. |

|

|

Source: Intro-act, JD Supra

SPACs liquidating faster this year than in 2022. We’re less than halfway through the year, but nearly $30 billion from so-called “blank check” companies has already been returned to investors. That’s about 50% ahead of the pace set in 2022, when a whopping $45 billion from special-purpose acquisition companies, or SPACs, got liquidated and sent back home, according to data compiled by SPACInsider, an industry research firm. High profile investors like venture capitalist Chamath Palihapitiya, private-equity billionaire Alec Gores, former Goldman Sachs COO Gary Cohn and big Wall Street firms such as KKR & Co. and TPG Inc. have all liquidated their SPACs and returned money to investors as the number of available companies to buy plummets. Read More (New York Post)

IOSCO tackles SPAC boom concerns. The boom in SPACs may have subsided for now, but the possibility that their popularity will rise again when market conditions improve has led global securities regulators to consider investor protection guidelines, reports Investment Executive. The International Organization of Securities Commissions (IOSCO) published a report examining the SPAC phenomenon. The report also reviews the efforts of regulators in different markets to address SPAC risks through traditional disclosure and gatekeeper obligations. “While SPACs pose similar risks to investors as traditional IPOs, the complexity and uncertainty inherent in the SPAC structures raise a number of different risks,” the group said. Read More (Investment Executive)

Ripples following the SPAC wave: litigation and regulatory risks. It’s a pattern we often see in boom-and-bust cycles—disputes rising in the period after a wave crests. SPAC deal volume hit an unprecedented high in 2021, but then slowed down in 2022 alongside IPOs. However, the fallout from the SPAC wave will continue to unfold this year, generating increased regulatory attention and a growing number of disputes. The beginning of 2023 saw a new 1% excise tax applicable to certain SPAC redemptions go into effect under the Inflation Reduction Act. This year is also certain to see various SEC rule proposals take further shape. Predictably, the increase in activity and media attention and the follow-on regulatory focus have also inspired a surge in disputes. These disputes have given rise to further developments in the case law surrounding SPACs, some of which may increase the risk of and posed by new disputes moving forward. Read More (Private Fund Litigation)

Company insiders made billions before SPAC bust. The SPAC boom cost investors billions. Insiders in the companies that went public were on the other side of the trade. Executives and early investors in companies that went public via special-purpose acquisition companies sold shares worth $22 billion through well-timed trades, profiting before share prices collapsed. Some of the biggest winners were Detroit Pistons owner Tom Gores’s investment firm Platinum Equity, British billionaire Richard Branson and convicted Nikola founder Trevor Milton. They were among many insiders who got shares on the cheap and sold them as they rose in value, according to a Wall Street Journal analysis of insider-trading disclosures associated with more than 200 companies that did SPAC deals. Companies that went public this way have lost more than $100 billion in market value. At least 12 have filed for bankruptcy and more than 100 are running low on cash, battered by higher interest rates and rising costs. Read More (The Wall Street Journal)

|

Chart 6: Total Value of Stock Sold by Insiders at Companies that Went Public via SPAC Deals |

|

|

Source: Intro-act, The Wall Street Journal

Several AI-related companies going public via SPAC. So far this year, several AI-focused companies have announced tie-ups with SPACs, or special-purpose acquisition companies. Planned mergers span sectors including education, diagnostics and data management, CrunchBase reports. In addition, there are some AI-affiliated blank-check companies that have yet to identify an acquisition target. In this category, the most closely watched is AltC Acquisition, a $450 million SPAC that lists OpenAI co-founder and CEO Sam Altman as CEO. AltC went public in July 2021, with plans to identify an acquisition target within two years. Unless it gets an extension, that time is nearly up. Read More (Crunchbase News)

SilverBox takes unique approach to SPACs. Austin-based SilverBox Capital hopes to change the industry’s perception of SPACs by simply focusing on better targets, reports Mergers & Acquisitions. SilverBox’s focus on profitability pre-dates the SPAC boom-and-bust. “There are probably some great ideas that should be funded, but they shouldn’t be funded in the public markets,” says Joe Reece, SilverBox’s co-founder and co-managing member. “We’re not venture capitalists. We’re happy to bet on execution but we won’t bet on technology. We won’t fund things that are unproven.” Reece goes on to explain that the team’s ideal target is either profitable or has positive EBITDA, however they will consider companies that don’t meet this target if they can verify a genuine path to profitability. Read More (Mergers & Acquisitions)

In-house, law firms diverge on SEC rulemaking impacts. In a recent Bloomberg Law survey, concerns about the additional burden of cybersecurity and privacy rulemaking far and away led the list of impacts for in-house attorneys but ranked lower for law firm lawyers, who see disclosure obligations affecting their practices the most. Bloomberg Law’s State of Practice Survey asked 802 lawyers about the surge in SEC rulemaking under current Chair Gary Gensler and how these proposed and enacted new regulations are likely to affect legal practices and the clients, companies, or funds they advise. The results lend credence to the age-old story of more regulation leading to higher burdens on the regulated (and their legal counsel)—but those impacts land differently on the practices of in-house and law firm attorneys, according to the survey. Read More (Bloomberg Law)

SPAC Litigation: A review of recent developments. SPAC-related disputes have thus far focused on alleged conflicts of interest and the accuracy of disclosures regarding targets’ business prospects, and those issues are likely to continue to play a leading role as more motions to dismiss are decided, note lawyers with Jones Day, writing in JD Supra. While only a few decisions have been issued by the Delaware Court of Chancery so far, the standard of review applied in those cases is likely to have a significant impact on outcomes if adopted in other cases. Unlike the Delaware lawsuits, SPAC-related cases in federal court usually involve claims under Section 10(b) or 14(a) of the Exchange Act, although state law claims may also be asserted. The timing of the alleged misstatements and the roles of the individual defendants are important issues that may influence whether such claims survive at the pleading stage. Read More (JD Supra)

Court dismisses post-SPAC class action for lack of standing. On March 31, 2023, U.S. District Judge Ronnie Abrams of the Southern District of New York dismissed a putative securities class action against CarLotz, Inc. (CarLotz), and certain of its officers and directors on the grounds that plaintiffs lacked standing to sue for losses allegedly arising from false and misleading statements defendants made about CarLotz while it was still a private company. In 2021, CarLotz became a publicly traded corporation through a de-SPAC transaction whereby it merged with, and assumed the public registration of, the special purpose acquisition company (SPAC) Acamar Partners Acquisition Corporation (Acamar). Plaintiffs had purchased shares of Acamar prior to the de-SPAC transaction and later purchased shares of the post-merger, public CarLotz following the de-SPAC. Read More (JD Supra)

Mountain Crest faces lawsuit over Better Therapeutics SPAC deal. A Better Therapeutics Inc. shareholder sued the architects of its blank-check transaction, claiming the deal’s lopsided structure gave insiders a huge windfall despite virtually wiping out public investors. The lawsuit targets the Mountain Crest Capital LLC affiliates who engineered the $187 million merger between Better Therapeutics and a special purpose acquisition company. Mountain Crest and its principals are serial SPAC sponsors whose previous ventures include the blank-check deal that took Playboy public. Read More (Bloomberg Law)

Tishman Speyer, billionaire co-founder face SPAC deal challenge on Latch Inc. Tishman Speyer Properties affiliates, including billionaire co-founder Jerry Speyer, were hit with shareholder litigation Tuesday challenging the blank-check merger they engineered between smart lock startup Latch and TS Innovation Acquisitions almost two years ago. The lawsuit also targets the real estate giant’s CEO, Rob Speyer, and other backers of the SPAC that combined with Latch to take it public, Bloomberg reports. It accuses them of duping investors into a disastrous deal because the transaction’s lopsided structure gave them a huge windfall even if non-insiders were wiped out. Latch is the developer of the enterprise software-as-a-service (SaaS) platform LatchOS. Read More (Bloomberg Law)

Momentis lays off 60% of workforce a year after $1 billion SPAC deal collapse. Israeli surgical robotics company Momentis, formerly Memic, is laying off 60% of its employees. Following the layoffs, only 50 employees will remain at the company, which until recently had 120 employees. Around 40 of the remaining employees are based in Israel, with the rest headquartered in the U.S., CTECH reports. MedTech Acquisition in March 2022 called off its $1B merger agreement with the company, citing poor market conditions. The transaction terms had called for Memic, as the company was known at the time, to receive MedTech’s $250 million cash held in trust and a $76 million PIPE. Read More (CTECH)

Guide to D&O insurance for SPAC IPOs, 2023 edition. As they go through their initial public offering (IPO) and the subsequent merger & acquisition (M&A) process, special purpose acquisition companies (SPACs) face many regulatory, legal, and business hurdles. Obtaining the appropriate amount and type of insurance for each stage of their life cycle is one of them. However, with some smart preparation and the expertise of the right advisors, insurance can go from being a necessary burden to a strategic asset. Read More (JD Supra)

SPAC ETF (SPC) hits new 52-week high. For investors seeking momentum, CrossingBridge Pre-Merger SPAC ETF SPC is probably on radar. The fund just hit a 52-week high and is up 3.78% from its 52-week low price of $20.42/share. The fund seeks to provide total returns consistent with the preservation of capital, using an active investment strategy. A special purpose acquisition company (SPAC) raises capital through an IPO to acquire a private operating business within a specified timeframe. The product charges 80 bps in annual fees. In Q1, the volume of SPAC IPOs and mergers reverted to the pre-hype levels. The number of SPAC IPOs saw a slight increase compared to the second half of 2022, due to recent developments such as extensions, deal announcements, and liquidations, which helped to reduce the pressure of the SPAC maturity wall. Read More (Yahoo! Finance)

Super Group’s blank-check backers hit with SPAC deal challenge. An investor sued architects of the blank-check merger between online gambling company Super Group and a shell entity, claiming they duped shareholders into approving a lousy deal that made insiders rich, Bloomberg reports. The lawsuit targets the finance and sports industry veterans – including former senior executives at Goldman Sachs & Co. and the NFL – who sponsored Sports Entertainment Acquisition, the SPAC that combined with Super Group to take it public. Super Group operates the digital sports betting platform Betway and Spin, an online casino. Approved by the SPAC’s shareholders in January 2022, the transaction was expected to generate approximately $202.4 million – less than half the amount originally anticipated when the deal was announced last year. Redemptions hit 55% of shares outstanding ahead of the merger vote. Read More (Bloomberg Law)

Richard Branson’s Virgin Orbit to liquidate, being sold for parts. Stratolaunch and Rocket Lab USA are among the buyers for assets of Virgin Orbit Holdings, the bankrupt space-launch company tied to billionaire Richard Branson. Virgin Orbit will sell its modified Boeing 747, known as Cosmic Girl, to Stratolaunch for $17 million after no better bids emerged, according to bankruptcy court papers filed Tuesday, Bloomberg reports. Meanwhile, Rocket Lab is buying Virgin Orbit’s primary rocket factory in California for $16.1 million. Rocket Lab completed its business combination with Vector Acquisition in August 2021. Rocket Lab USA received approximately $777 million on the SPAC deal. Virgin Orbit’s bankruptcy represents a spectacular implosion of the once-promising space systems company, at one time widely touted as the next great innovator in advancing space travel. Read More (Bloomberg)

Freightos freezes hiring plan as it absorbs SPAC costs. High SPAC costs, and public scrutiny in a “cynical” market has clouded Freightos’ Q1 results, resulting in a hiring freeze, even as the company tried to focus on its record growth, The Load Star reports. Revenues rose nearly 10% year-on-year, to $4.8 million, but the company, which has only announced its results publicly in the last two quarters since listing, made a loss of $49.28 million, compared with a loss of $4.2 million a year earlier. However, noted Freightos, the SPAC and listing cost some $46.7 million, while another $3.7 million went on transaction-related costs, essentially accounting for the entire loss. Read More (The Loadstar)

Payment’s processor Plastiq files for bankruptcy after aborted SPAC deal. Payment’s processor Plastiq has filed for bankruptcy, less than a year after an aborted merger with a special-purpose acquisition company and weeks after Silicon Valley Bank’s collapse temporarily halted its operations. San Francisco-based Plastiq sought protection from creditors with a proposed deal to be acquired by publicly traded payments business Priority Technology Holdings. Since its 2012 founding in a Boston apartment until 2021, Plastiq raised $142 million in funding and was once valued at $550 million. Read More (The Wall Street Journal)

Trump Media files $3.78 billion defamation lawsuit against Washington Post over Truth Social reporting. The company behind Donald Trump’s Truth Social platform has filed a $3.78 billion defamation lawsuit against the Washington Post. The lawsuit, filed by Trump Media & Technology Group in Florida’s Sarasota County, claims that a May 13 article that alleged the company may have committed securities fraud was false and defamatory, and posed an “existential threat,” The Independent reports. Read More (AoI)

Trump’s Truth Social faces more trouble: SEC calls SPAC’s financial statements unreliable as stock faces delisting. Digital World Acquisition, which plans to merge with the parent company of Donald Trump’s Truth Social platform, reported it made accounting errors in its last financial report, adding to financial reporting issues that have threatened to delist the company from Nasdaq, on top of two investigations that have delayed the deal with Trump. The year-end report can “no longer be relied upon,” Digital World told regulators, and the company is now developing a remediation plan to address the “material weakness” in its “internal control over financial reporting,” per the filing. Read More (Forbes)

As deadlines loom, SPACs strike array of pacts with health firms. Deal-needy SPACs have struck a series of pacts to take small health-care companies public as they race against the clock to avoid the risk of forfeiting the money they raised. Since early April, at least nine health firms — predominantly medical device makers and drug developers – have agreed to mergers to go public via U.S. special purpose acquisition companies, accounting for roughly 40% of the deals announced in that period. EnGene Inc., a biotech company, and Avertix Medical Inc., maker of a device that can detect heart attacks, are among the most recent SPAC deals in the healthcare industry. Read More (Bloomberg Law)

Crypto firms eye public listings as markets rebound. The 2023 market rebound is enabling some crypto companies to explore an option that appeared off the table just six months ago: trying to go public. Bitcoin-mining company Bitdeer Technologies listed on the Nasdaq last month after merging with a SPAC, a blank-check company so called for its use in helping businesses access public markets with fewer strings attached. Blockchain company Chia Network recently took another step toward going public, while cloud-mining company BitFuFu and crypto cash-machine company Bitcoin Depot are working on plans to go public via SPAC mergers. Read More (Financial News)

America’s SPAC-funded NewSpace industry is crashing due to gov’t regs and high capital costs. An array of NewSpace companies were funded through billions raised through SPACs and venture financing and are at the cutting edge of providing new and cheaper space products. In the launch industry, these include ABL, Astra, Firefly, Relativity Space, Rocket Lab, and Virgin Orbit are producing low-cost rockets. In the earth observation industry, Planet Labs competes with satellites from big defense contractors in photo-reconnaissance and Capella Space with a constellation that provides low-cost radar imaging. Axiom is building commercial space stations. The exciting innovation, competition, expansion of the U.S. industrial base, deepening of supply chain and jobs these companies bring provides America the boost it needs to stay ahead of adversaries and bring down defense costs. That’s the good news, reports Space News. Read More (Space News)

Space could be a $1 trillion-dollar business. Here are the stocks to play it. SpaceX’s Starship isn’t the only space-related blowup recently. Space stocks, too, have crashed, and while most are never coming back, a couple might be worth buying out of the wreckage. It wasn’t that long ago when space was the next big thing in the stock market. Two years ago, special purpose acquisition companies, or SPACs, were all the rage—and space stocks used the vehicles to go public. Companies including Astra Space (ticker: ASTR), which provides launch services; Earth observation company Spire Global (SPIR); and Momentus (MNTS), the FedEx of space, all came public with much fanfare—and now trade for less than a buck. Read More (Barron’s)

Record-breaking SPAC deal for EV firm shows market weakness, not strength. A record-breaking SPAC deal to bring a Vietnamese electric-vehicle maker to market showcases just how distorted things have become in the industry. VinFast is going public with a $27 billion enterprise value through a tie-up with the special-purpose acquisition company Black Spade Acquisition Co., which raised a modest $169 million in a July 2021 initial public offering. That valuation-to-IPO ratio of almost 160 times would be the largest ever, a Bloomberg analysis of SPAC Research data show. The median this year is one-and-a-half times. Another signal of the discrepancy between the valuation and Black Spade’s cash is that even if there are no redemptions, the EV firm’s existing shareholders are set to own 99% of the company, leaving a tiny portion for SPAC investors who hold on through the deal. Read More (Yahoo! Finance)

Routes to the public markets in Canada: IPO, SPAC, CPC or RTO. In general, two routes exist for a PrivateCo to go public – an initial public offering (IPO) of securities or a negotiated reverse merger transaction (RMT) with an existing public company. The IPO process centers on the creation of a public company from a PrivateCo. An IPO may be accomplished by either a marketed listing of securities of PrivateCo or a direct listing of PrivateCo's securities on a stock exchange. Alternatively, a RMT involves the acquisition of a PrivateCo by an existing public company (typically a shell or inactive company), resulting in the shareholders of the PrivateCo ultimately owning a majority of the shares of the resulting public issuer (resulting issuer), which subsequently carries on the business of the PrivateCo. A RMT may be accomplished by one of three means: (1) an acquisition of PrivateCo (a QA or qualifying acquisition) by a special purpose acquisition corporation (SPAC), (2) an acquisition of PrivateCo (a QT or qualifying transaction) by a capital pool company (CPC), or (3) a reverse takeover (RTO) of an existing public company. Read More (JD Supra)

|

Chart 7: Summary Comparison of IPOs, SPACs, CPCs and RTOs |

|

|

Source: Intro-act, JD Supra

London’s first SPAC, Hambro Perks, de-Lists from exchange. Hambro Perks Acquisition Company – London’s first SPAC – has de-listed, according to a regulatory filing. HPAC said it cancelled its official listing with the Financial Conduct Authority and on the main market for listed securities of the London Stock Exchange, Investment Week reports. The company had suspended its own shares on May 2 following a delay in the publication of its annual report and financial statements for the year ended Dec. 31. At the time, HPAC said it had also entered liquidation. In April, Hambro Perks co-founder and CEO Dominic Perks quietly left the venture capital firm and stepped down as director of the SPAC. Read More (DealFlow’s SPAC News)

UK SPAC deal derailed on claims of abusive

investor behaviour. A SPAC merger that was set to bring a UK steel

distributor public has been cancelled after allegations of abusive behaviour by

purported shareholders in the blank check firm. The SPAC tie up that would’ve

resulted in Megasteel Ltd. going public later this year was called off after

groups claiming to be investors in the acquirer, More Acquisitions PLC,

approached the target’s management and owners using “abusive and threatening

behaviour.” The “unwarranted tirade of abuse and vitriol directly addressed” at

Megasteel’s owners and board led the company to withdraw its merger agreement. The

SPAC at deal announcement last year said Megasteel is valued at between GBP49.5

million to GBP63 million on completion of the acquisition. Read More (Bloomberg

Law)

SunCar Technology Group Inc. (SDA) and Goldenbridge Acquisition Limited complete business combination. SunCar Technology Group Inc., a leading provider of digitalized enterprise automotive after-sales services and online auto insurance intermediation service in China, completed its business combination with Goldenbridge Acquisition Limited (Nasdaq: GBRG), a publicly traded special purpose acquisition company. The business combination was approved at a special meeting of Goldenbridge’s shareholders on April 14, 2023. Beginning Thursday, May 18, 2023, SunCar’s Class A ordinary shares and warrants started tarding on the Nasdaq Capital Market under the ticker symbols “SDA” and “SDAWW,” respectively. Read More (Globe Newswire)

Tigo Energy, Inc. (TYGO) and Roth CH Acquisition IV Co. complete business combination. Roth CH Acquisition IV Co. (Nasdaq: ROCG), a publicly-traded special purpose acquisition company, completed its business combination with Tigo Energy, Inc., a leading provider of intelligent solar and energy storage solutions. The business combination was approved by ROCG shareholders in a special meeting held on May 18, 2023, and formally closed. The combined company will operate under the name “Tigo Energy, Inc.” and will be led by Tigo’s senior management, who will continue to serve in their current roles. Commencing at the open of trading on May 24, 2023, Tigo’s common stock started trading on Nasdaq under the ticker symbol “TYGO.” Read More (Business Wire)

Enocean terminates merger agreement with Parabellum. PropTech SPAC Parabellum Acquisition Corp. (OTC: PRBM) announced that energy harvesting IoT specialist, EnOcean GmbH had terminated their merger agreement. EnOcean, based in Germany, looked well-positioned to become a successful publicly listed company. The firm is a pioneer of energy-efficient IoT devices for commercial buildings and smart spaces. It maintains extensive OEM partnerships with more than 350 product manufacturers and is a founding member of EnOcean Alliance, a non-profit international association of companies that promotes interoperable eco-systems for smart homes, smart buildings and smart spaces with over 300 members. Read More (memoori)

SuperBac Walks away from XPAC acquisition deal. XPAC Acquisition in an 8-K disclosed that its merger partner SuperBac on May 2 told the SPAC it was terminating the deal. The decision was based on multiple factors, according to the filing, including unfavorable market conditions and trends in share price performance of recent de-SPAC companies, heightened volatility and share price risks and the fact that no PIPE investments had been entered into that would provide sufficient funds. Anticipated PIPE financing from Modal Yorkville had not been secured. Lacking those funds, SuperBac indicated the minimum cash condition could not be met. While XPAC has until Aug. 3 to sign and seal a new deal, the SPAC said in the regulatory filing that the more likely outcome will be liquidation if shareholders approve. Read More (SEC)

Better World Acquisition abandons Heritage Distilling deal. Better World Acquisition in an 8-K said it terminated a merger agreement with Heritage Distilling, but offered no reason as to why. At deal announcement in December, the ESG-focused SPAC said it would combine with the craft distiller at a pro forma enterprise value of $122.2 million. Washington State-based Heritage offers a variety of whiskeys, vodkas, gins and rums produced mainly from local, sustainably sourced ingredients. To accelerate its national wholesale distribution growth strategy, Heritage founded the Tribal Beverage Network to collaborate with Native American tribes to serve patrons of tribal casinos and entertainment venues. Better World has two months remaining on its current deadline extension. Read More (SEC)

German family-owned Schmid Group aims for SPAC listing on NYSE. Germany's Schmid Group said it plans to list in New York via a special purpose acquisition company (SPAC), in a deal estimated to give the technology firm a valuation of $640 million. The fifth-generation family-owned business, which specialises in electronics, would become a publicly-listed company on the New York Stock Exchange in the fourth quarter of this year. Founded as an iron foundry in 1864 and headquartered in Freudenstadt in Germany's Black Forest, Schmid has more than 800 employees and develops equipment and manufacturing processes for printed circuit boards, as well as technology for industries including renewable power and energy storage. Read More (Reuters)

Abu Dhabi investment firm to list SPAC – Only the second in the Middle East. An investment firm backed by Abu Dhabi’s Al Maskari family is planning to list a blank-check firm in the city. This would be the second such deal in the Middle East. MEASA Partners is targeting a listing for the SPAC this year, the people said, asking not to be identified as the information isn’t public. It’s working with Abu Dhabi Commercial Bank PJSC and Credit Suisse Group AG on the potential listing, they said. Abu Dhabi Catalyst Partners, a joint venture between Mubadala Investment Co. and Alpha Wave Global, is expected to anchor the transaction. Details of the offer such as its size and timeline are still preliminary and subject to change, while more banks may be added at a later stage, they said. Read More (Bloomberg)

|

Chart 8: SPAC Events – June 2023 (1/2) |

|

S. No |

Event Name |

Date |

Time |

|

1 |

SHUA Deadline extension vote |

6/1/2023 |

9AM EST |

|

2 |

ROC Deadline extension vote |

6/1/2023 |

11:30AM EST |

|

3 |

CONX Deadline extension vote |

6/1/2023 |

12PM EST |

|

4 |

EFHT Deadline extension vote |

6/1/2023 |

12PM EST |

|

5 |

WEL Deadline extension vote |

6/2/2023 |

10AM EST |

|

6 |

BIOS Deadline extension vote |

6/2/2023 |

11AM EST |

|

7 |

FRLA extension contribution amendment vote |

6/2/2023 |

12PM EST |

|

8 |

TGAA Deadline extension vote |

6/2/2023 |

12PM EST |

|

9 |

MTAL & CSA Copper Mine (Glencore subsidiary) Power Merger Vote |

6/5/2023 |

9AM EST |

|

10 |

LBBB Deadline extension vote |

6/5/2023 |

10AM EST |

|

11 |

IPVF Deadline extension vote |

6/5/2023 |

12PM EST |

|

12 |

AVAC & Beneficient Merger Vote |

6/6/2023 |

10AM EST |

|

13 |

BOCN Deadline extension vote |

6/6/2023 |

10AM EST |

|

14 |

KVSA Deadline extension vote |

6/6/2023 |

10AM EST |

|

15 |

RONI & NET Power Merger Vote |

6/6/2023 |

11AM EST |

|

16 |

PMGM & AEON Biopharma Merger Vote |

6/6/2023 |

12PM EST |

|

17 |

TCOA Deadline extension vote |

6/8/2023 |

10AM EST |

|

18 |

HAIA Deadline extension vote |

6/9/2023 |

9AM EST |

|

19 |

PORT Deadline extension vote |

6/9/2023 |

10AM EST |

|

20 |

XPDB Deadline extension vote |

6/9/2023 |

11AM EST |

|

21 |

BRAC Deadline extension vote |

6/9/2023 |

3PM EST |

|

22 |

MEOA & Digerati Technologies Merger Vote |

6/12/2023 |

9AM EST |

|

23 |

SHAP Deadline extension vote |

6/12/2023 |

9AM EST |

|

24 |

MTAC Deadline extension vote |

6/12/2023 |

9AM EST |

|

25 |

PRLH Deadline extension vote |

6/12/2023 |

10AM EST |

|

26 |

PLAO Deadline extension vote |

6/12/2023 |

10AM EST |

|

27 |

BFAC Deadline extension vote |

6/12/2023 |

11AM EST |

|

28 |

IVCP Deadline extension vote |

6/12/2023 |

3PM EST |

|

29 |

LFAC Deadline extension vote |

6/13/2023 |

11AM EST |

|

30 |

ATEK Deadline extension vote |

6/13/2023 |

1PM EST |

|

31 |

EDTX Deadline extension vote |

6/13/2023 |

1:30PM |

|

32 |

CFFS Deadline extension vote |

6/14/2023 |

10AM EST |

Source: Intro-act, SPAC Track, Boardroom Alpha

Chart 8: SPAC Events – June 2023 (2/2)

|

S. No |

Event Name |

Date |

Time |

|

33 |

EVE Deadline extension vote |

6/14/2023 |

11AM EST |

|

34 |

RCAC Deadline extension vote |

6/14/2023 |

11AM EST |

|

35 |

COOL Deadline extension vote |

6/15/2023 |

1PM EST |

|

36 |

FLFV Deadline extension vote |

6/16/2023 |

11AM EST |

|

37 |

GDNR Deadline extension vote |

6/20/2023 |

10AM EST |

|

38 |

VII Deadline extension vote |

6/20/2023 |

12PM EST |

|

39 |

THCP Deadline extension vote |

6/21/2023 |

2:30PM EST |

|

40 |

CFIV Deadline extension vote |

6/22/2023 |

10AM EST |

|

41 |

VHAQ Deadline extension vote |

6/22/2023 |

10:30AM EST |

|

42 |

MCAF Deadline extension vote |

6/22/2023 |

10:30AM EST |

|

43 |

MCAG & AUM Biosciences Merger Vote |

6/23/2023 |

10AM EST |

|

44 |

ADEX Deadline extension vote |

6/30/2023 |

10AM EST |

Source: Intro-act, SPAC Track, Boardroom Alpha

|

Chart 9: SPAC Activity by Month |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 10: Current Status of the SPAC Universe |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 11: Current Status of SPAC Universe by Trust Size |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 12: SPAC Transactions by Year |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 13: Average SPAC IPO Size ($ Mn) |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 14: SPAC Transactions by Month (LTM) |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 15: Time to Liquidation – By Volume |

|

Chart 16: Time to Liquidation – By Trust Value |

|

|

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 17: Active SPACs By Sector (As of Month Ending May 2023) |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 18: Average Redemption Rate by Month |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 19: SPAC Redemption Detail – May 2023 |

||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

|

Chart 20: Monthly SPAC Activity – May 2023 |

|

|

Source: Intro-act, Boardroom Alpha. Searching figures ($Mn and Count) are as of month end.

|

Chart 21: SPAC IBC Announcements by Target Sector – May 2023 (1/2) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

Chart 21: SPAC IBC Announcements by Target Sector – May 2023 (2/2) |

||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

The SPAC and New Issue ETF (SPCX). SPCX gives investors exposure to a broad portfolio of SPACs with the familiar attributes of an exchange traded fund’s diversity, tax efficiency and liquidity. SPCX is the first actively managed SPAC ETF. Why active? As the SPAC market is rapidly evolving, we believe that the portfolio management approach should equally reflect the dynamic nature of this burgeoning capital-raising alternative. This is no place for a rigid rules-based index strategy.

|

Chart 22: SPCX Summary Data |

|

Chart 23: SPCX Top 10 Holdings |

||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||

Source: Intro-act, ETF.com. Data as of 5/31/23.

|

Chart 24: SPCX Performance |

|

|

Source: Intro-act, Yahoo! Finance. Data as of 5/31/23.

|

Chart 25: Relative-SPAC Index vs Russell 3000 |

|

|

Source: Intro-act, FactSet

|

Chart 26: Gainers and Losers in the Broader SPAC Universe (% Change) |

|

|

Source: Intro-act, FactSet

|

Chart 27: SPAC IPO Pricings by Sector – May 2023 |

||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

|

Chart 28: SPAC S-1 Filings by Sector – May 2023 |

||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

|

Chart 29: SPAC Institutional Owners League (Current) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, 13F Filings

|

Chart 30: DE-SPAC Institutional Owners League (Current) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, 13F Filings

|

Chart 31: SPAC Underwriter League (YTD As of May 2023 End) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research. Note: Credit for Bookrunner Volume ($ Mn) is based on the total amount of the offering sold, including over-allotment. Full credit is awarded to the sole book-runner or split equally among joint book-runners.

|

Chart 32: Top De-SPAC Advisors (YTD As of May 2023 End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research. Note: Advisor credit is shared equally among all advisors on a given deal, as a proportion of the enterprise value of the target company acquired by the SPAC. Firms with multiple advisory roles receive credit for each role.

|

Chart 33: SPAC Legal League (YTD As of May 2023 End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research. Note: Credit for Volume ($ Mn) is awarded to both Issuer and Underwriter Counsel.

|

Chart 34: SPAC Auditor League (YTD As of May 2023 End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research

|

Chart 35: ICR – The Leading SPAC Communications and Capital Markets Advisor |

|

113 Transactions / $267 Billion in Transaction Value Since 2021

|

Source: Intro-act, ICR. Announced SPAC transactions since 2021, All Announcements not shown. Data as of April 2022.

Analyst Certification

I, Peter Wright, certify that the views expressed in the research report accurately reflect my personal views about the subject securities or issues. I also do not receive direct or indirect compensation based on my recommendations or views.

Intro-act, Inc. (Intro-act) issued this report and may seek fees for the assistance with investor targeting, access, and further investor preparation services. Intro-act, Inc. will not seek renumeration for any investment banking service or investment advice.

Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources who are believed to be reliable. However, the issuer and related parties, as well as Intro-act, do not guarantee the accuracy or completeness of this report, and have not sought for this information to be independently verified. Opinions contained in this report represent those of the Intro-act analysts at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, and estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties, and other factors that may cause the actual results, performance, or achievements of their subject matter to be materially different from current expectations.

Exclusion of Liability: To the fullest extent allowed by law, Intro-act, Inc. shall not be liable for any direct, indirect, or consequential losses, loss of profits, damages, or costs or expenses incurred or suffered by you arising out or in connection with the access to, use of, or reliance on any information contained in this note.

No personalized advice: The information that we provide should not be construed in any manner whatsoever as personalized advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Intro-act’s solicitation to affect, or attempt to affect, any transaction in a security. The securities described in the report may not be eligible for sale in all jurisdictions or to certain categories of investors.

Investment in securities mentioned: Intro-act has a restrictive policy relating to personal dealing and conflicts of interest. Intro-act, Inc. does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees, and contractors of Intro-act may have a position in any or related securities mentioned in this report, subject to Intro-act’s policies on personal dealing and conflicts of interest.

Copyright: Copyright 2023 Intro-act, Inc. (Intro-act).

Intro-act is not registered as an investment adviser with the Securities and Exchange Commission. Intro-act relies upon the “publishers’ exclusion” from the definition of investment adviser under Section 202(a) (11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Intro-act does not offer or provide personal advice, and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell, or hold that or any security, or that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person.